Charity incorporation FAQ

Next – some questions that are top of our minds. (Note: our good friend ChatGPT helped with this research, and we validated as much as possible manually.)

1. Can an unincorporated charity employ staff?

In the UK, unincorporated charities do not have a separate legal personality. As a result, they do not have the capacity to employ people directly in their own name. However, unincorporated charities can still engage individuals to work for them by using alternative arrangements, such as employing them as individuals or through a contracting arrangement. These individuals would not be employed by the charity itself, but rather by the trustees or a separate employing entity.

It is important to note that employing individuals through these alternative arrangements may have implications for tax, employment rights, and other legal considerations. It is advisable for unincorporated charities to seek professional legal and financial advice to ensure compliance with relevant employment and tax laws when engaging individuals to work for the organisation.

2. How much would it cost to incorporate?

Legal Fees: Engaging a solicitor or legal professional to guide you through the incorporation process and handle the necessary legal documentation can incur fees. The cost may depend on the complexity of the charity’s structure and any additional legal services required.

Registration Fees: There may be fees associated with registering the incorporated charity with the relevant regulatory body. In the case of charities in England and Wales, this would involve registering with the Charity Commission.

Accounting and Financial Reporting: As an incorporated charity, you may need to engage an accountant or financial professional to manage your financial reporting obligations. The cost may depend on the complexity and size of the charity’s finances.

Other Administrative Costs: Incorporation may involve various administrative tasks, such as updating governing documents, notifying stakeholders, and potentially reorganizing assets or contracts. These activities may have associated costs, such as printing and mailing expenses.

3. What running costs do we need to consider?

- Accounting and Bookkeeping: Engaging a professional accountant or accounting firm to handle the charity’s financial records, bookkeeping, and financial reporting can cost anywhere from £1,000 to £5,000 or more per year, depending on the complexity of the charity’s finances and the level of service required.

- Independent Examination/Audit: An incorporated charity may be required to have its financial statements independently examined or audited, depending on its income and legal obligations. The cost of an independent examination or audit can range from £500 to £5,000 or more, depending on the size and complexity of the charity’s finances.

- Software and Technology: Investing in accounting software or financial management systems can incur costs. Depending on the software chosen and the organisation’s needs, costs can range from £100 to £1,000 or more per year.

- Payroll Management: If the charity has paid employees, it may require payroll management services to handle payroll calculations, tax deductions, and reporting. The cost of payroll management services can vary depending on the number of employees and the complexity of payroll requirements. Generally, costs can range from £500 to £2,500 or more per year.

- Training and Professional Development: Ongoing training and professional development for staff or trustees involved in financial management can be beneficial. Costs for training programs or courses can vary widely, ranging from £100 to £1,000 per person or more, depending on the nature and duration of the training.

- Insurance: It is advisable for incorporated charities to have appropriate insurance coverage, such as professional indemnity insurance, which can help protect against potential financial risks. The cost of insurance premiums can vary depending on the size of the charity and the coverage required.

Our next Board meeting is in 10 days. We will be talking about these issues and – I hope – finally making a decision. My current thinking is that incorporation is a key part of the growth strategy of the organisation. But I think we could put in place some triggers that indicate exactly when we should make the change. Triggers could be related to the increasing liability faced by trustees e.g. our turnover growing to a certain amount, our membership growing to a certain number (and thus the liability increasing). They could also be related to the running of the organisation, for example, us needing to hire someone, or being awarded a grant that requires us to be incorporated.

What do YOU think?

A key part of leadership is being open to listen and change your mind. So – am I right? What do you think is missing from the above? If you’ve tackled these issues before, or would like to debate, please connect with me on LinkedIn or Twitter. I would love to hear what you think, and learn from the wisdom of others!

Thank you!

If you’d like to discuss an ethical communications strategy, how strategic decisions like this may affect your organisation (however big or small), or any of the topics above, please contact AMS. I’m also open to connecting on LinkedIn for a chat anytime!

Onward! ❤️

—

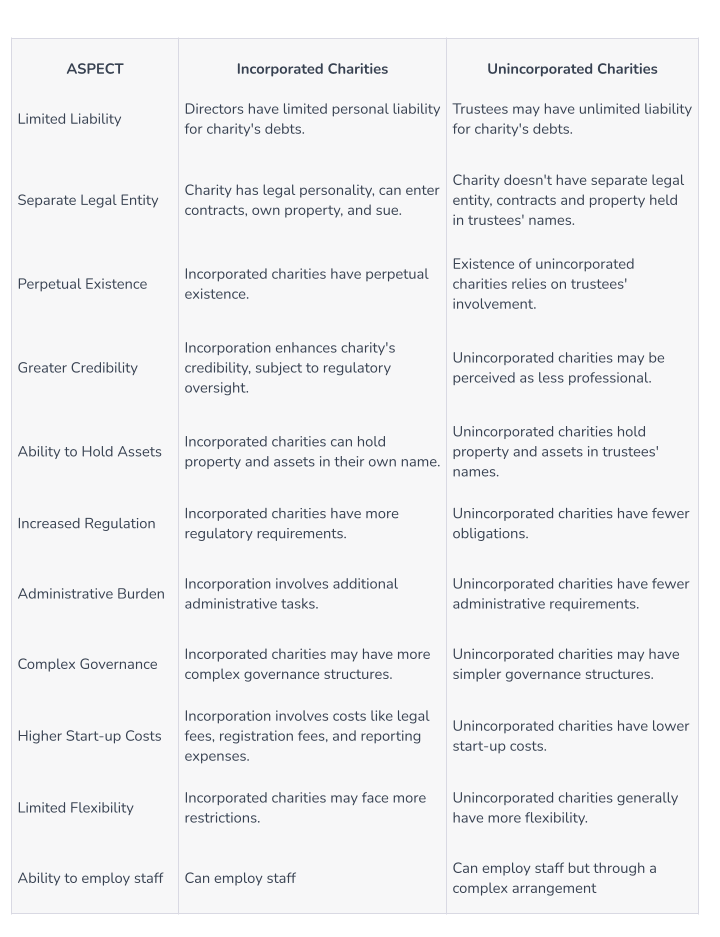

Text of table image – for screen readers

Limited Liability

Directors have limited personal liability for incorporated charity’s debts.

Trustees may have unlimited liability for unincorporated charity’s debts.

Separate Legal Entity

Incorporated Charity has legal personality, can enter contracts, own property, and sue.

Unincorporated Charity doesn’t have separate legal entity, contracts and property held in trustees’ names.

Perpetual Existence

Incorporated charities have perpetual existence.

Existence of unincorporated charities relies on trustees’ involvement.

Greater Credibility

Incorporation enhances charity’s credibility, subject to regulatory oversight.

Unincorporated charities may be perceived as less professional.

Ability to Hold Assets

Incorporated charities can hold property and assets in their own name.

Unincorporated charities hold property and assets in trustees’ names.

Increased Regulation

Incorporated charities have more regulatory requirements.

Unincorporated charities have fewer obligations.

Administrative Burden

Incorporation involves additional administrative tasks.

Unincorporated charities have fewer administrative requirements.

Complex Governance

Incorporated charities may have more complex governance structures.

Unincorporated charities may have simpler governance structures.

Higher Start-up Costs

Incorporation involves costs like legal fees, registration fees, and reporting expenses.

Unincorporated charities have lower start-up costs.

Limited Flexibility

Incorporated charities may face more restrictions.

Unincorporated charities generally have more flexibility.